Options Strategies (WAO Part 3)

--

In the third part to my Options series, What are Options?, I will be telling you some strategies one can perform using options other than buying singular calls (bullish) and puts (bearish).

With just the singular calls, you typically want to buy calls to increase leverage while maintaining or decreasing the total possible loss amount. For example one can either buy 100 shares of JPM @ $150 for a total cost of $15,000 or one can buy one 145C JPM expiring in a couple months for $700. With the latter, a 5% or $7.5 increase in the underlying results in a gain of ~78.57% for the call option or a profit of $550. Now sure this is less than the $750 you’d get if you used $15,000, but my point is how you can use options to increase leverage without using more capital, so if you had invested your other $14,300 wisely, you’d rake in more profit (but might end up losing more money in a market-wide downturn).

If the stock had gone down at least 5%, buying the call option would’ve actually saved you money, since 5% of $15,000 is $750 > $700. This argument only works though if you had kept the other $14,250 at bay and not fully invested.

Volatility impacts the price of options a lot, so make sure you are aware of how volatility may increase or decrease in the time period till your contracts expire. Earnings are just one of many catalysts that may affect price action and volatility.

Without further ado, here are some options strategies that may open your eyes or push you into thinking differently.

Covered Calls (CC)

I mentioned selling covered calls in part 1, but I want to get into it a bit more.

If you are ever long on a stock but want some extra income/interest, you can sell covered calls on it. You will need to own the at least 100 shares and each contract you write/sell would represent the obligation to sell 100 shares at the strike price you sold the contract at until the expiration date of the contract, at which point the contract either expired worthless, you closed the contract, or you were assigned.

Ideally you don’t want to sell a call with an expiration date that is too close (weeklies) that you’d get almost no premiums from with the risk of assignment. It is very easy for cheap contracts to 3x in value in the span of a week, so there’s no point in selling them especially when you can sell the next weeks contract for more time value. Since weekly options are close to their intrinsic value, selling in the money (ITM) calls can be useful if you want to either close out your position or are anticipating some downturns in the coming days. To get out of my $NIO position, I buy to close (BTC) the August call I had written and sell to open (STO) a $2 ITM call expiring in 2 days. I actually got too impatient and ended up STO a strike price $2 less than my original order which would’ve been filled if I had just waited a couple of hours. It’s not that big of a deal since I had written multiple covered calls before on $NIO.

For a moderately volatile stock, you’d want to sell a covered call that expires in a couple of weeks where the time value/day peaks and the theta decay will start to eat the premiums. This ends up being ~3 weeks to 30 days to expiry (DTE). Which expiry you choose to sell (if at all) depends on each stock just because each stock behaves differently. Be aware of short-term upwards momentum due to earnings, and other events. I had sold a covered call on $NIO before NIO day and that’s why I had to roll my covered call all the way till August... Rolling is when you BTC the call you wrote and STO another call simultaneously so that you can still own the stock. It won’t work well if the call is way ITM. With respect to the calls you had written, calls that expire later with higher strike prices drop less percentage points on a down day and therefore you are looking for a down day to roll your calls further out and an up day to roll your calls closer.

The strike price you pick should be a price you are willing to sell at in the short-term since a too big of a strike price will actually give you pennies per share. Aim to get at least 1% a month in premiums and no more than 9% unless you want to get assigned. Make sure to have an assignment plan such as rolling as I said above or just taking the opportunity loss.

The first covered calls I ever sold were some high Implied Volatility (IV) calls on $INO. I ended up selling covered calls 3 times over 3 months reducing my cost basis by $3 before the stock become more than just a stock I was neutral on and I more of a stock I was biased on, preventing me from selling it and even selling more covered calls when it almost doubled in value. I was down on the stock itself for most of the 3 months, but the covered calls definitely covered the unrealized losses, so I was not worried unlike other bag holders I’m sure the stock had created.

Some brokerages will let you purchase the stock and sell the covered call all in one order. I personally try to buy the stock on a down day and then wait a day before selling the covered call, in order to maximize gains if the stock happens to increase the next day.

I will not be mentioning selling naked calls because the losses are unlimited, the risk is too high for the profit, and the buying power required is high. I don’t doubt some people do it though, since as we saw before, this guy had sold naked puts on oil and left them open while on Vacation.

Cash Secured Puts (CSP)

If you ever wanted to get in on a stock but are worried about any short-term downwards movement, selling puts is a great way to lower your cost-basis while earning something. Start off by choosing a strike price of the stock you’d like to purchase. For me this would be CRSR @ $35. Now, just like with the covered calls, pick an expiration date 3 weeks from now to 30 days. It is also helpful to write the cash covered puts on a down day, since the premiums on puts will be higher.

I won’t be talking about married puts, where you short a stock and then write a put to cover your short just because shorting shares is taking a risk of unlimited losses.

I do however support selling naked puts that are covered with cash which can only be done in a cash/margin account. Notice how I said cash covered. It is imperative that the puts you wrote if assigned would not use margin. This is because if the stock goes well below the strike price of the put, your brokerage can margin call you even if the puts haven’t been assigned to you yet and even then you could get margin called.

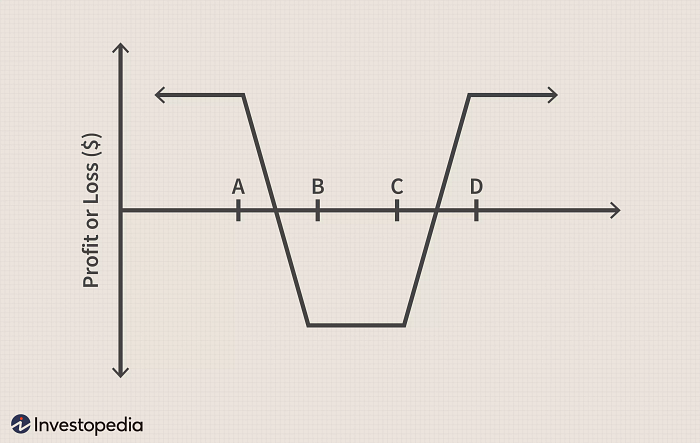

Straddles & Strangles

Going long on a straddle means buying both a call and a put option for the same underlying stock, with the same strike price and expiration date. A long strangle is just lie a straddle but with differing strike prices.

Going short would just mean selling the call and put instead of buying them.

Use Cases

Long Strategy

- Volatile underlying (positive or negative trend) suggest larger price swings and larger profits.

- You may want to take advantage of volatility by buying straddles in anticipation that volatility will increase due to a company’s earnings report coming up, or you may try to take advantage of the decrease in volatility after a company has released their earnings report.

Short Strategy

- Betting that underlying will stay flat (low volatility)

- Unlimited risk, see long call butterfly for limited risk

Spreads

Spreads basically involve BTO options and STO the same type of options.

Spreads are for active investors. You must pay close attention to your account or be able to keep up to date with your emails so that in cases where you get assigned on the short, you can exercise the long, assuming your broker didn’t logically do it for you.

With all spreads, make sure you close your position before the market closes on the day of expiry. This will ensure you don’t get assigned while unable to exercise your long position, which would open you up to more losses than you bargained for.

Bull Call Spread

Also called a debit call spread, this strategy Simultaneously BTO and STO two different strike priced calls with the call you are buying at a lower strike price than the call you are writing, hence the debit. The expiration dates are the same.

The maximum profit is the difference between the strike prices minus the initial debit and the maximum loss is the initial debit. One might want to open a debit call spread if they are more bullish on a stock than just holding shares but not bullish enough to only BTO a call.

One might even employ this strategy if they wanted to limit their downside. Instead of buying a call with a stop loss, one can buy a spread with the debit being the max amount you are willing to lose. This is great if you don’t want to deal with the stress of losing and cutting losses.

Poor Man’s Covered Call

Now if you wanted to employ a covered call strategy but don’t have enough capital to buy 100 shares of the stock you want to runt the strategy on, have no fears, for you can BTO an ITM long-dated call and STO an OTM shorter-dated call.

Bear Call Spread

Also called a credit call spread, this strategy is the exact opposite of the strategy above. Simultaneously BTO a call with a strike price higher than the strike price of the call you STO (expiration date remaining constant). This will credit your account. The credit is the maximum profit and the maximum loss is the difference between the strike prices minus the initial credit.

Bull Put Spread

Also called a credit put spread, this strategy consists of two put legs, simultaneously BTO a put with a strike price lower than the put that you STO, (expiration date remaining constant). This will result in a credit to your account since the higher strike price put is worth more than the lower strike price put. You usually want both puts to be OTM to lower the probability of being assigned. The maximum profit is the credit you received and your maximum loss is the difference between the strike prices.

Bear Put Spread

Also called a debit put spread, this strategy consists simultaneously BTO a put with a strike price higher than the put you STO (expiration date remaining constant). This will be a debit to your account. The maximum profit is the difference between the strike prices minus the initial debit. The maximum loss is the debit you paid.

Diagonal

A Diagonal is an option spread but with different expiry dates and differing strike prices, hence the term “diagonal.” The Poor man’s covered call employs a call diagonal. With diagonals, you want to watch out for the cases where the short leg has no long leg protecting against “tail risk.” In such situations, you either want to have enough buying power to take assignment or you want to buy an appropriate long leg to reduce your risk to something more tolerable. It is also possible for your brokerage to completely liquidate your position in such a scenario if your entire margin excess gets sucked up.

Long Butterfly

A butterfly involves 4 options of the same type.

Call Butterfly

A long call butterfly involves buying 1 ITM call, selling 2 at the money (ATM) calls, and buying 1 OTM call, resulting in a debit. One would employ this strategy when they think the underlying won’t move much. Opening this strategy is much less riskier than a short straddle, and the maximum profit equals

ATM strike price - ITM strike price - initial debit. Maximum loss is equal to

OTM strike price - 2 * ATM strike price + ITM strike price.

A short call butterfly just doesn’t make any sense since you are opening a credit spread that’s already at risk of being assigned and also a debit spread, that’ll need the underlying to up by the premium just for you to break even on it. Just open a debit spread with higher strike prices or buy a straddle since you are betting on movement.

Put Butterfly

A put butterfly is similar to a call butterfly but instead of using calls, one uses puts (BTO and STO remains the same). The use case is the same: to profit off neutral action.

A short put butterfly makes no sense either and buying a straddle instead is much better.

Iron Butterfly

An iron butterfly consists of a bear call spread and a bull put spread. STO an ATM put and an ATM call, BTO an OTM put and an OTM call. Maximum gain is the net credit received and the maximum loss equals the greater of the differences in strike price of the call spread or the put spread.

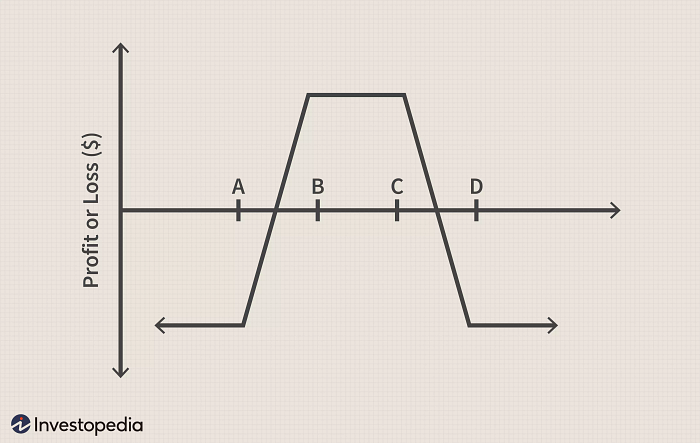

Condor

All condors consists of a 4 legs, and a profit zone which is the price range between the second lowest strike price and the second highest strike price.

Call Condor

A long call condor consists of 4 call legs. BTO an ITM (below profit zone) call, STO a call at the bottom of your profit zone, STO a call at the top of your profit zone and BTO a call above your profit zone. The initial debit will be less than the difference between the bottom two strike prices because the two calls with higher strike price are a credit spread.

The use case and goal is for the underlying to stay between the second lowest strike price call and the highest strike price call so that one of the short legs expires worthless and the ITM call is worth more than the initial debit paid. One is short volatility but with less risk as compared to a butterfly which requires the underlying to expire at a specific price for the maximum profit.

The maximum profit equals: (Second Lowest Strike Price - Lowest Strike Price) - Initial debit and is achieved as long as the underlying closes between the strike prices of the two short calls.

It is more simple to buy a straddle than to open a short call condor. Anyways, here is that profit diagram (covered under fair use thankfully).

Put Condor

A put condor works the same way as a call condor but one uses puts in the places of calls. The BTO and STO remains the exact same for the strike prices selected.

Iron Condor

Finally the last strategy: The Iron Condor. Similar to the last two strategies, this strategy profits off of underlying neutrality. The difference is the that it is composed of two puts and two calls. The lower legs is a bull put spread and the upper legs is a bear call spread. Like the two other spreads, maximum profit is achieved if the underlying closes between the middle strike prices, in which case all legs expire worthless and you get to keep the initial credit.

An example would be:

- Sell 1 AAPL Apr 120 put

- Buy 1 AAPL Apr 110 put

- Sell 1 AAPL Apr 130 call

- Buy 1 AAPl Apr 140 call

- Maximum loss (risk) = $10 ×100=$1,000

- Maximum profit = initial credit

Implied Volatility Strategies

IV is a huge indicator to find options and stocks that the market finds interesting. It took me ~6 months to come up with the first strategy which was to sell high IV covered calls. Barchart is what I use to find interesting stocks and options to sell covered calls on. I wish it was as simple as picking the first stock in the list but I do a lot of research into the companies.

In particular, I look at if I know of the company, the stock price has to be at least $7 (out of penny stock territory), stock must not have been “pumped” or have recently surged, to reduce downside potential. I’m not interested in cannabis stocks mainly because their financial situation and long term graph do not make them attractive even in the short term. I’m sure my opinion on them will change as some are slowly becoming stable.

In times where some stocks are trending hard + my constraints, this scanning strategy will barely yield a single interesting stock. A very important note with this strategy is to always bare in mind that you bought the stock to sell covered calls and nothing else. It is very easy to start “believing” in a stock even if it is performing well for now.

Another strategy that I have not followed through with yet, but might do so in the future, is IV Rank and Percentile. Barchart has this table of stocks with their respective ATM IV, the ATM IV compared to its highest and lowest values over the past year, and the % of days in the past year where ATM IV has closed lower than the current ATM IV.

To play the IV Rank, one needs to speculate on catalysts of IV increase. For example AAPL, its only 14.45% of the highest IV it’s been at. The highest was either because of a market down-turn, an Apple event, earnings, etc. I don’t believe playing the IV Rank is useful for buying options in anticipation of an increase in IV but it can prove to be useful to play it to selling options in anticipation of a decrease in anticipation.

A high IV Rank does not imply that IV will actually decrease in the same time span of your options since an extremely high IV Rank could also stay at 100% if the IV continues to increase, which is possible. So when you do play it make sure you aren’t selling naked positions, and I definitely wouldn’t be selling cash secured puts either. A better idea is to sell covered calls on stocks that have a high IV Rank due to simply trending upwards. Be sure to have an exit strategy since these will definitely be a short-term play.

Percentile tells us more information about how a stock’s IV will move in the future. A high percentile would indicate that most days have lower ATM IV and a low percentile indicates that most days have a higher ATM IV. One can use this to buy or sell options in anticipation of an IV increase/decrease based on probability. You would be speculating on the days till an IV move and usually non-directional (straddles), meaning there’s a huge risk, especially if the IV moves every once in a while instead of daily.

It’s much better to use these two IV tables to find interesting stocks to sell covered calls / CSP on rather active options speculation which will lead to major losses without risk management.

Conclusion

That wraps up my What are Options? series. I hope these three parts have you made you a more informed investor.

As always, if there was something I did not explain correctly, please leave feedback, so that I can improve the article.